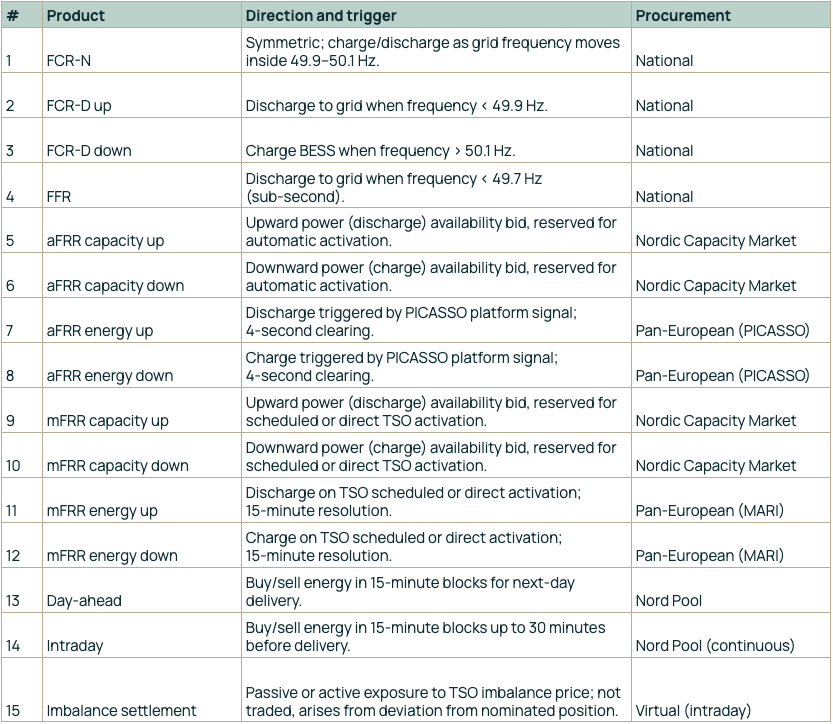

.jpg)

From the 1.2 MW Suvilahti BESS commissioned in 2016 to the 125 MW investment decisions in 2026, the Finnish utility-scale BESS merchant business case has gone from individual R&D market participation to multi-market trading via 15 market mechanisms. This post provides an overview how a merchant BESS makes money and how we got here.

A merchant BESS in Finland can earn from 15 distinct market mechanisms. Some are national, some Nordic, some pan-European. Some clear day-ahead, some every four seconds. A BESS trader i.e. an optimizer running on top of the battery decides constantly where the capacity and energy go.

As of today, Finland has only one TSO, Fingrid, and operates as one pricing zone. It is good to understand that even though Fingrid is working hard to mitigate the issue, there is pressure to create several pricing zones due to geographic imbalances between onshore wind on the western side and industrial electrification in the southern side of Finland, while simultaneously CHP plants are being decommissioned in many high-demand areas.

As of Q2/2026, the following sources of revenue are available for BESS:

The optimizer forecasts price levels across these markets and allocates capacity to maximize gross profit. It should account for the sanction regime (non-delivery costs roughly 3× the market price in ancillary services) alongside grid variable cost, energy cost, warranty-based cycle limits and other potential limitations. Choosing which markets to bid into is a constant trade-off between expected revenue, risk, and wear.

Finland’s reserve markets developed after the Nordic day-ahead electricity market had already become the core wholesale price and scheduling mechanism. Finland joined the Nordic power market in 1998, and day-ahead trading became the main commercial baseline for next-day electricity delivery. Reserve markets then evolved around that baseline.

Initially Finnish TSO Fingrid procured reserves through long-term bilateral contracts with a handful of large industrial consumers and power plants (mostly hydro and thermal). Prices were negotiated, not market-determined, and participation was closed to everyone else.

Competitive auction-based ancillary service and reserve procurement started 14 years ago. Most of today's markets were introduced during the 2020s, and procurement volumes are still growing.

Timeline of Ancillary Services in Finland

2012: FCR-N and FCR-D up launched as competitive markets: annual tender plus hourly top-up, pay-as-cleared, national only.

Jan 2013: aFRR introduced Nordic-wide as a coordinated TSO-level product. No separate capacity market yet; allocation via Nordic SOA distribution key.

May 2020: FFR launched as a national hourly market, sub-second response product for low-inertia situations.

Nov 2021: Nordic single price imbalance settlement adopted by all four TSOs.

Jan 2022: FCR-D down launched as a new traded product; procurement ramped gradually toward full obligation.

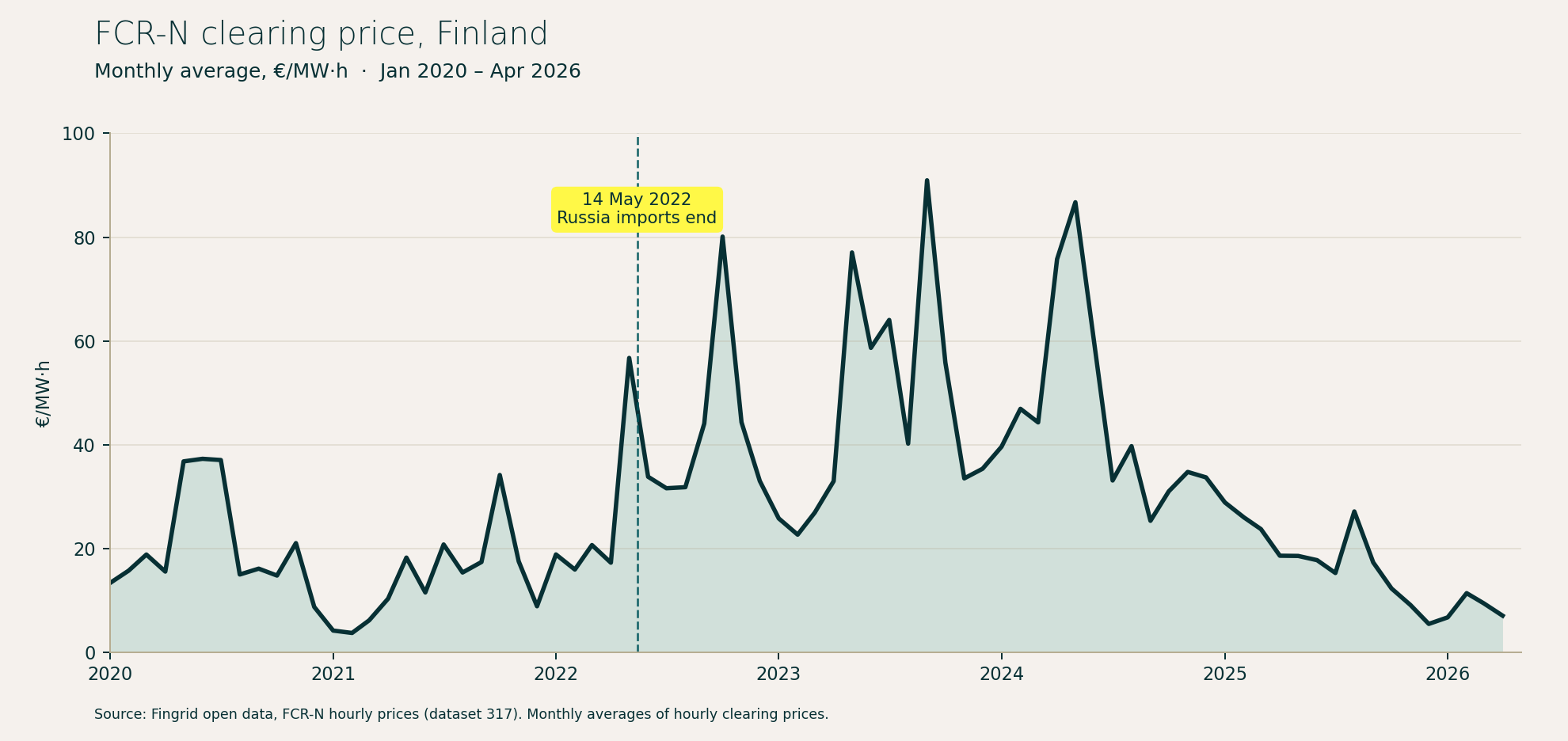

14 May 2022: All electricity trade and reserve procurement from Russia ends. Fingrid had been importing ancillary services from Russia which stopped overnight.

Aut 2022: Finnish mFRR capacity market reformed to D-1.

Dec 2022: Nordic aFRR capacity market live, daily D-1 auction, pay-as-cleared, cross-border capacity reserved.

Jun 2024: Finnish aFRR energy market launched locally, 4-second MTU, precursor to PICASSO.

Oct 2024: Nordic flow-based cross-zonal capacity calculation adopted.

Nov 2024: Nordic mFRR capacity market expanded to cover Sweden and Denmark on a shared IT platform.

Mar 2025: mFRR energy activation (MARI) live across all four Nordic TSOs, automated dispatch, 15-minute resolution.

Mar 2025: Finland joins PICASSO, aFRR energy now pan-European, 4-second clearing.

May 2025: Finland-Estonia PICASSO trading started via EstLink 1.

One date matters more than the rest: 14 May 2022 when all electricity trade and reserve procurement from Russia ended. Fingrid had been importing ancillary services across the border. That supply disappeared overnight.

The consequence was a structural jump in reserve prices in 2023 and 2024. That, combined with the first wave of project developments and a sharp fall in battery capex, produced the BESS investment boom we see today. Finland went from around 200 MW of stand-alone BESS capacity at the start of 2025 to more than 1 GW in 2026, with additional projects already under construction.

The boom has moved faster than most expected, and batteries increasingly set the marginal price in these pay-as-cleared auctions. Revenue levels have fallen slightly faster than the early financial models assumed.

Power-reserve revenues have peaked. Energy-market revenues from day-ahead, intraday, aFRR energy and mFRR energy markets are rising. The underlying driver is a structural increase in Finnish electricity demand.

Montel Analytics already describes Finland as Europe's most volatile short-term electricity market. The reason is a binary generation mix: large nuclear (including the 1.6 GW Olkiluoto 3 unit that came online in 2023) on one side, fast-growing wind on the other (approx. 10 GWp already). When the wind blows hard, prices collapse to near-zero or negative. When nuclear is down for maintenance and wind drops, prices spike above 300–400 €/MWh.

Finland currently consumes around 9 GW on average and peaks around 14 GW in winter. Over 2 GW of data center capacity and over 2 GW of district-heating electric-boiler capacity are now past investment decision and mostly under construction, with more projects queued. Hydrogen, e-fuels, green steel, and general industrial process electrification add further upward pressure on demand over the medium term.

More demand, a fixed interconnection envelope, and continued wind and solar build-out driven by that same demand point to structurally higher average prices and wider intraday and day-ahead swings. That is a good environment for batteries earning on energy arbitrage.

Beyond the 15 markets listed above, new revenue pools are opening. DSOs are piloting local flexibility market. More sources are likely to emerge as volatility increases, the grid gets more congested and more granular flexibility products are designed around these issues.

As project sizes grow, so does the importance of de-risking the described merchant exposure. That is a topic in its own right, and the subject of a separate future post.

If you are interested in our investment thesis on how to monetize the increasing volatility in European power markets, see our investor page.

We believe in long-term partnerships, but also cherish new beginnings.